Repayment Options

Federal Student Loan Repayment Plans

These are the traditional plans for paying off federal student loans.

Standard Payment Plan

You are given this repayment plan automatically. You will pay a fixed amount per month.

- Pro: You'll pay off your loan faster.

- Con: Your monthly payment might be high.

Graduated Payment Plan

The graduated plan gives you a low monthly payment in the beginning, then increases your payment amount every two years.

- Pro: You'll pay less per month to start.

- Con: Your monthly payments will increase even if your income doesn't.

Extended Payment Plan

Your monthly payments are lower, over a longer period. Payments can be a fixed or graduated amount.

- Pro: You'll pay less per month.

- Con: You'll pay more in interest and it will take longer to pay off your loans.

Income-Driven Plans

These plans provide payment amounts that are dependend on your post-grad income.

Interest Rate: Depending on the selected plan, you'll pay between 10% and 20% of your discretionary income toward your loans each month.

Discretionary Income: For income-based repayment plans and loan rehabilitation, discretionary income is the difference between your income and 150% of the poverty guideline for your family size and state of residence.

Timing: Loan balance will be forgiven after making on-time payment for 20-30 years.

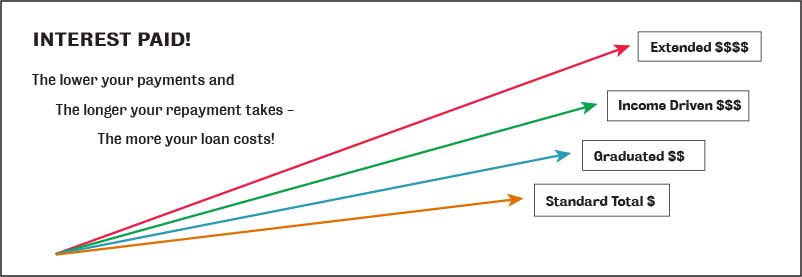

Repayment Examples

The loan repayment chart above shows cost comparison between repayment plans.

The lower your payments and the longer your repayment takes, the more your loan costs due to higher interest paid.

Here is an example is based on the average Direct Loan debt for an FIT student: $21,000 in loans at an interest rate of 3.9% for someone who is single and living in New York with an income of $34,000 and with a yearly increase of 5%.

| Repayment Plan | First Monthly Payment |

Last Monthly Payment |

Total Interest Paid |

Repayment Period |

Total Paid |

|---|---|---|---|---|---|

| Standard | $212 | $212 | $4,394 | 120 months | $25,394 |

| Graduated | $118 | $355 | $5,481 | 120 months | $26,481 |

| REPAYE (Revised PAYE) | $135 | $275 | $5,611 | 133 months | $26,611 |

| PAYE (Pay as you earn) | $135 | $212 | $5,756 | 143 months | $26,756 |

| Income based | $202 | $212 | $4,445 | 121 months | $25,445 |

| New Income-Based | $135 | $212 | $5,756 | 143 months | $26,756 |

| Income-Contingent | $145 | $172 | $6,842 | 177 months | $27,842 |

We suggest that you go to your loan servicer's website, create a login and password for your account, and then use their loan repayment calculator to get estimated repayment amounts based on your current Direct Loan debt.

If you do not know who your servicer is, log into NSLDS (National Student Loan Data System) with your FSA ID and passwordand then click on one of your loans.

Tips

Sign up for automatic debit payments with your loan servicer and receive an interest rate deduction.

Change your repayment plan if you have difficulty making payments. You aren't stuck with your original plan.